Introduction

This newsletter provides a snapshot of the performance of Greek hotels based on a sample of more than 180 hotels & resorts in Greece. The hotel performance data is complemented by data from other sources so as to place the Greek hospitality industry in the context of Greek tourism and of the International Hospitality Industry. Finally, the outlook of the industry, as seen by hoteliers themselves, is given.

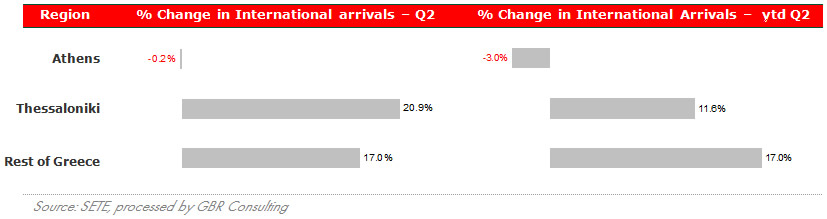

International arrivals1 in Greek airports, 2011 compared to 2010

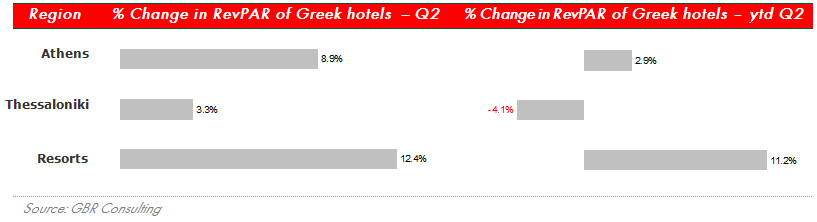

RevPAR2 in Greek hotels, 2011 compared to 2010

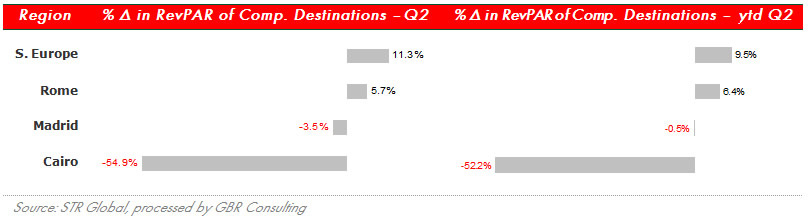

RevPAR in Competitive Destinations, 2011 compared to 2010

Commentary

- International arrivals by air really picked up in the second quarter of this year, with Thessaloniki and the rest of Greece seeing substantial increases of 20.9% and 17.0% respectively in Q2, while Athens stabilised. As a result the YTD numbers turned positive as well, while Athens improved from YTD Q1 of -8.3% to -3.0% in YTD Q2.

- In terms of RevPAR the developments for Athens and Thessaloniki were also positive with an increase of 8.9% for Athens compared to -4.3% in Q1 and 3.3% for Thessaloniki compared to -11.1% in Q1. The resort hotels opened their doors in Q2 and showed excellent performance with an increase of 12.4% in RevPAR compared to Q2 of 2010, resulting in a YTD of 11.2%. According to the 2011 Q3 Barometer of GBR Consulting, resort hoteliers are bullish for Q3 regarding occupancy, while for ARR prospect the outlook ranges from stable to slightly optimistic.

- Compared to the data from the Southern European hotels, it is the first time since this newsletter started being published, that Greek hotel performance compares favourably.

Hotel & Other News

- Airotel is one of the few chains continuing to expand in city destinations; it has just opened its 7th hotel in the city of Kavala, 150 room Galaxy Hotel, approximately 1 year after opening the Smart Hotel in Patras. Its expansion plans are based on concepts suitable for the current economic climate.

- The Porto Hydra resort was acquired by the Restis family (shipowners).

- According to a report of the Hellenic Statistical Authority in July 2011 there was a spectacular increase comparing foreign arrivals of Q1 2011 with 2010 from France (+70.5%), Russia (+79.8%) and Turkey (+97.8%), while arrivals from Britain rose by 32.4% and from the US by 16.6%. On the other hand there was a decline of 19.5% in arrivals from Germany and 15.9% from Cyprus.

- Besides the increased number of arrivals so far in 2011, one can say that the tourism industry as a whole strengthened in 2011, mainly due to a) the reduction of VAT for hotels, enhancing their competitiveness, b) simplified procedures for travel documents, particularly boosting Russian arrivals and

c) partial lifting of restrictions for the cruise industry (albeit, still much needs to be done).

- Finally, the BoD of the newly-formed Privatisation Fund of Greece has been appointed. It plans to privatise ~ € 50 billion of publicly owned assets in the next 5 years, the vast majority of which will be real estate assets, many of them of a predominantly tourism character. Among them is the site of the old international Athens airport at Elliniko, plots at Anavyssos in south-eastern Attika, Mesolongi in western Greece, Vathy on the island of Samos, the Kaiafas Springs in the Peloponnese, Prasonisi island just south of Rhodes etc.

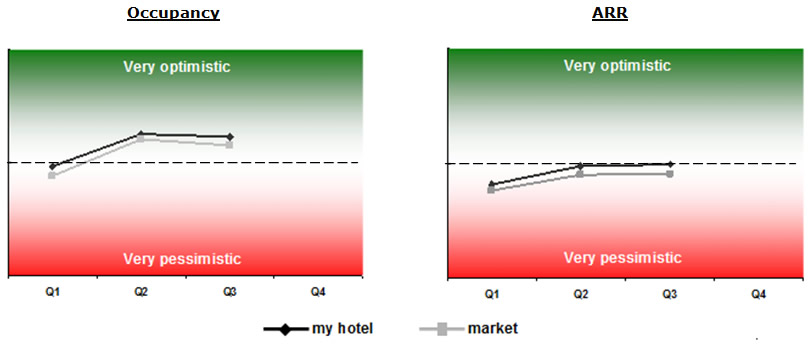

Barometer

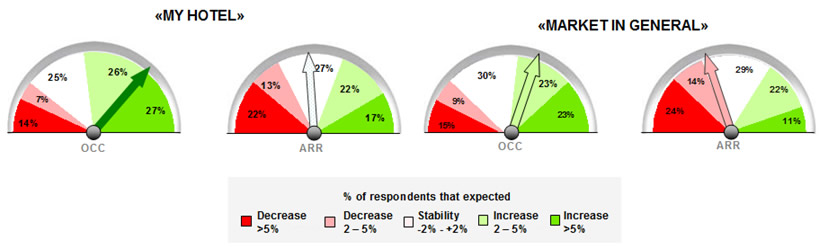

- In our Tourism Barometer survey for 2011 Q3, hoteliers remain optimistic for their occupancy development following expectations in Q2, while forecasts for ARR vary from slightly negative to stable as we have also seen in the previous quarters. The outlook for “my hotel” is still better than for the “market in general”.

- The most optimistic hoteliers in Q3 are from Crete, expecting increases in occupancy levels as well as in prices. Next most optimistic group is the 5 star hoteliers. The 3 star hoteliers on the other hand are the most pessimistic of the entire Q3 survey, expecting sharp drops in occupancy as well as ARR. Hoteliers in Thessaloniki expect the biggest drop in ARR.

- The graphs below show that after a sharp increase in optimism in Q2 the barometer expectations for occupancy have stabilised in Q3. With respect to ARR, hoteliers remain slightly pessimistic for Q3, but at the same level as for Q2.

Endnotes

1 The international arrivals statistics are based on SETE calculations compiling the data from 13 major airports of Greece, representing 95% of foreigners' arrivals by plane in Greece and 72% of total foreigners' arrivals. Thessaloniki airport does not distinguish between arrivals of Greeks and foreigners.

2 RevPAR : Revenue per Available Room; for Greek resorts, calculations are based on TRevPAR (i.e. Total RevPAR). |