Introduction

This newsletter provides a snapshot of the performance and outlook of the Greek hotel industry, within the broader context of the international hospitality industry as well as of Greek tourism and Greek socio-economic developments.

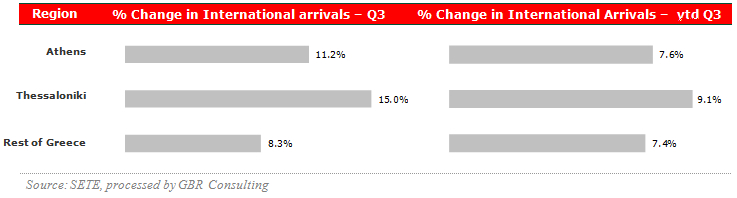

International arrivals1 at Greek airports, 2016 compared to 2015

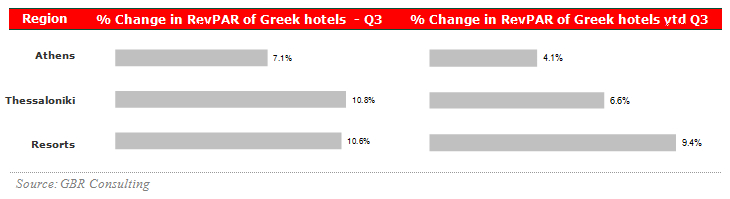

RevPAR2 in Greek hotels, 2016 compared to 2015

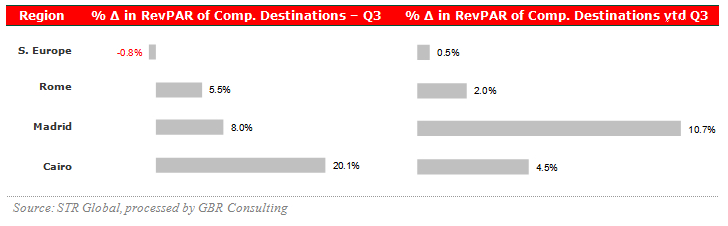

RevPAR in Competitive Destinations, 2016 compared to 2015

Commentary

- International arrivals at Greek airports showed a robust Q3 with an increase of 9.3% y-o-y. September was particularly strong with an increase of 13.2% y-o-y. However, arrivals on the islands of Kos and Lesbos dropped by 13% and 57% respectively up to Q3 2016, while Rhodes increased their arrivals with 9.3%. Also the main airports of Crete, the Ionian Islands and Cyclades showed increases in international arrivals up to September of 11.3%, 12.2% and 10.1% y-o-y.

- In line with the increase of arrivals at the Athens International airport, occupancy improved during Q3 after a difficult H1. Room rates improved 4.5% y-o-y YTD Q3 2016. In Thessaloniki occupancy levels increased with double digit numbers during Q3, while room rates slightly declined in comparison to the same quarter in 2015. Resort hotels in Greece improved their performance compared to last year based on an increase of 9.4% y-o-y of Total Revenue per Available Room up to Q3 2016. However, the lower hotel categories face fierce competition and their TRevPAR dropped significantly.

- We must note that expectations, after the record year of 2015, were too high at the beginning of the season in some destinations, especially in Santorini and Mykonos. That does not mean that they had a bad year though.

- On an international level Southern Europe performed on par so far with last year in terms of RevPAR. However, there significant differences between Mediterranean countries. The Spanish and Portuguese hotel sectors improved their RevPAR with 13% and 12% y-o-y up to September 2016, while RevPAR over the same period declined in Turkey, France and Italy with 42%, 11% and -1.6% respectively.

Concerns on declining travel receipts

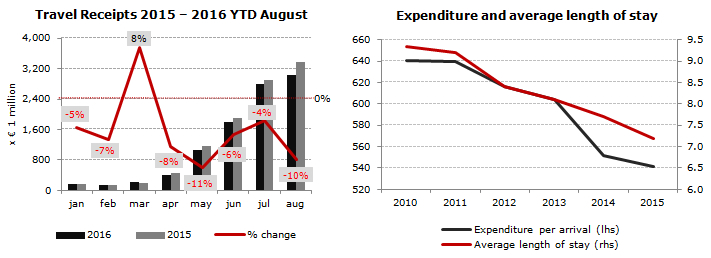

- Data of the Bank of Greece shows that tourist arrivals up to August increased with 1.8% compared to a year earlier, which is the result of increased arrivals by air and a small drop in arrivals by car.

- However, travel receipts dropped significantly. As shown in the graph, during the high season period of June – August receipts dropped by 6.8%, while August recorded a drop of 10% in comparison with a year earlier. The Greek tourism industry has started an intense discussion on the reasons, but without all the data of 2016 at hand one cannot make a full analysis.

- In our opinion the main reasons are:

- Shorter length of stay, which is a trend that is ongoing for the last decade. Also city break tourism with short lengths of stay has increased in Athens, Thessaloniki and other destinations.

- Arrivals from Balkan countries increased significantly during the past years, but are low spenders in compared with other European countries. Comparing 2010 with 2015 arrivals from Bulgaria nearly tripled, while arrivals from Romania and Albania more than doubled. In addition more than 3 million arrivals from FYROM were recorded in 2015.

- Especially the lower hotel categories and rooms to let units might have discounted their offerings in attempt to fill up their properties. We note that currently 56% of all hotels or 5,400 properties carry the 1 or 2 star categories.

- The UK pound has lost 18% of its value comparing the value at the beginning of the year with its current value. After the Brexit vote of June 23, 2016 expenditure of British tourists in Greece dropped by 36% in July, while arrivals dropped by 7.5% y-o-y. In August arrivals from the UK increased by 14%, while expenditure increased by just 0.5%.

- One cannot attribute the decline in travel receipts to platforms like AirBnB as this expenditure should be included in the border survey carried out by the Bank of Greece. So far the income is just not declared by the apartment / house owner. However, the Greek Government has prepared a draft law, which includes the registration of these properties, taxation up to 5% per overnight stay, limitations such as a maximum stay of 90 days that a property may be rented out (40 days on islands with less than 100,000 inhabitants), a maximum of 2 properties, fines etc.

Outlook

- In general the industry is concerned with the developments of the travel receipts, the ongoing refugee crisis and the financial status of hotel companies due to a high percentage of NPLs. More specifically, the Bank of Greece stated that 54.1% of all loans in the tourism sector are categorised as Non Performing Loan at the end of H1 2016, while the overall average in Greece was 45.1%. Sustainable solutions to cooperative borrowers must be developed and provided to resolve the issue.

- To remain competitive, the public and private sector must further invest in its infrastructure, minimise bureaucracy, liberalise various sub markets, further develop existing and new tourism products, increase competition between airlines to lower rates, develop a competitive tax system and implement a framework for the so called sharing economy (see above).

- For the medium and long term SETE, the Greek Association of Tourism Enterprises, has announced a new strategy towards 2021 as the goals of the previous strategy in terms of international tourist arrivals were achieved 5 years earlier. The new goals are set at 34.8 million tourists by 2021 and € 20 bn receipts, which means that expenditure per arrival is expected to stay at current levels. Around € 6.5 bn of investments are necessary to achieve these goals. The new strategy is again based on Greece’s main products Sun & Beach, City Break, MICE, Culture & Religion and Nautical, with a particular focus on the combination of various products. Medical tourism is no longer considered a main pillar.

Investment activities in Athens, but hotel stock remains stable

- Following the surge in demand, investment activity in the Athens hotel sector clearly picked up. However, the hotel stock in Athens has remained almost unchanged in the past 5 years as deals involve existing hotels and properties that have closed down still outnumber the new hotel developments. A quick overview of the main developments.

- Two major deals were finalised just a few days ago:

- The sale of the Asteras complex in Vouliagmeni to Apollo Investment Holdco for € 393 mn was signed last Thursday. Discussions are taking place with Four Seasons to take over the management. The franchise agreement with Starwood is expiring.

- The Athens Hilton was sold for € 142 mn to Greek company Home Holdings SA, a member of TEMES SA, and the Amsterdam-based D-Marine Investments Holding BV, a subsidiary of Turkish Dogus Holding. The transaction, which was also signed last Thursday, is subject to approval by the Greek Competition Commission. Furthermore, Home Holdings is in discussion with Mandarin Oriental Hotel Group for the operation of the hotel. The contract with Hilton expires.

- Marriott announced in October that it will return to Athens in 2018, as the 5-star Metropolitan Hotel located at Syngrou Avenue opposite the newly built Stavros Niarchos Foundation Cultural Centre will become the Athens Marriott Hotel with 366 rooms. Chandris Hotels, which currently owns and operates 5 hotels in Greece will proceed with a refurbishment of $ 15 million.

- A number of existing hotels changed hands and reopened or are scheduled to reopen soon:

- The 5 star Wyndham Grand Athens with 273 rooms will open its doors on the 1st of December. The hotel is located at Karaiskaki Square and formerly housed the Athens Imperial, which was closed in 2012.

- The public Aviation Fund is organising a public bidding in November this year for a 40 years lease of the former La Mirage hotel located at Omonia Square. The former 2 star hotel has 208 rooms, but is in need of renovation and must be upgraded to a 4 or 5 star hotel.

- Finally, as reported earlier, the 111-room Athens Tiare Hotel opened in July in a property known as the former 2 Fashion Hotel. - Arabian Somewhere Group acquired the 250 room Eden Beach.

- Over the past year new hotel developments added nearly 600 rooms to the Athens hotel stock, while other projects have been announced:

- In October the 5-star 216 room Electra Mitropolis opened at Mitropoleos Street and was the first hotel in Greece to receive a "LEED" certificate by the "US Green Building Council".

- In August the 4-star 94 room Athens Avenue Hotel opened at Syngrou Ave.

- And, as earlier reported, Domotel Kastri (86 rooms), Coco Mat Kolonaki (39 rooms) and a number of boutique hotels opened in the past year.

New projects are planned. N. Daskalontonakis – Grecotel is planning a 5 star hotel at a property at Mitropoleos Street close to Monasteraki. Approval for change of use of the listed building, owned by Chytiroglou and constructed in 1925, was given at the beginning of this year. Also two other buildings at Mitropoleos St are planned to be transformed into hotels.

The Merchant Seamen’s Fund, owner of a 7 storey building located in the centre of Athens at Akadimias Ave and Omiros St., is currently negotiating a lease agreement with the Yazbek Group, who has the intention to convert it into a luxury hotel.

- On the other hand many existing hotels remain closed. Only the following 4 properties have already 936 rooms together:

- The 5-star 314 room Athens Ledra Hotel for which a new auction will be organised in November

- The 5-star 210 room Acropol hotel at Omonio Square

- The 4-star 185 room Esperia Palace in Stadiou Street

- And the 3-star 126 room City Plaza hotel closed in 2010 and is now used by refugee families

- The 5-star 101 room Pendelikon remains closed for the time being

Latest developments

In Rhodes & Kos the following key developments were announced:

- Sani – Oaktree will open a new Ikos resort in Greece at the former Kefalos Kos Club Mediterranee resort, which has been closed for 4 years. In February of this year the ministry lifted a number of problems that existed on the modernisation and expansion of the hotel. Furthermore, the 298 room Ikos Oceania will be upgraded with a total budget of € 11.2 mn.

- The 4-star Louis Colossos Beach will be transformed into the 5–star Amada Colossos Resort. The renovation of the 697 room hotel - one of the largest hotels in Greece - is budgeted at € 45 mn. In addition Colossos SA has started the construction of a new 5-star resort in the same area of Kalithea in Rhodes. The new 222 room Marvel Luxury resort has an investment budget of € 25 mn. The company also operates the 59 room 5–star Rodos Park Suites & Spa.

- As earlier reported in our newsletter of Q1 the new 5-star Atlantica Dreams Resort will open in 2017 under the flag of Sensatori of Tui and will have 684 beds.

Other major developments announced this quarter are:

- Sani Group has started construction of Sani Dunes, a new 5-star 136 room hotel within Sani Resort, which is scheduled to open for adults and children above 12 in June 2017. The total investment is budgeted at € 24.2 mn. In addition Sani is investing € 13.3 mn for the upgrade and expansion of Sani Club, adding 46 junior suites and 16 suites with private pools.

- Two new tourism investments have been approved in October by the Ministry Economy, Development & Tourism and will be included in the fast track procedures. One project is known as the Eagle Resort, which is planned on the island of Evia, Karystos. The other project involves the construction of a 5-star tourist complex in Agios Nikolaos, Elounda - Crete by a consortium called Mirum Hellas.

Endnotes

1 The international arrivals statistics are based on SETE calculations compiling the data from 13 major airports of Greece, representing 95% of foreigners' arrivals by plane in Greece and 72% of total foreigners' arrivals. Thessaloniki airport does not distinguish between arrivals of Greeks and foreigners.

2 RevPAR : Revenue per Available Room; for Greek resorts, calculations are based on TRevPAR (i.e. Total RevPAR). |