Introduction

This newsletter provides a snapshot of the performance and outlook of the Greek hotel industry, within the broader context of the international hospitality industry as well as of Greek tourism and Greek socio-economic developments.

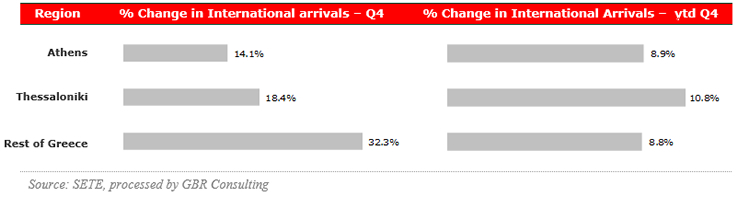

International arrivals1 at Greek airports, 2016 compared to 2015

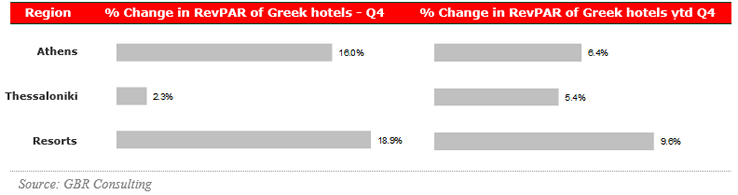

RevPAR2 in Greek hotels, 2016 compared to 2015

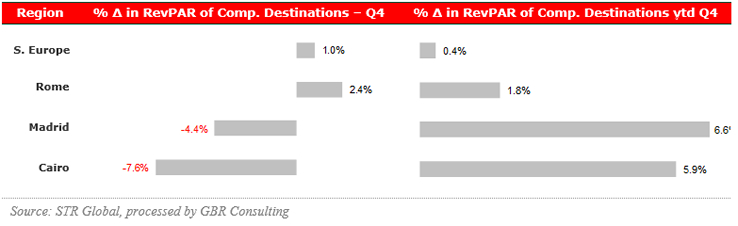

RevPAR in Competitive Destinations, 2016 compared to 2015

Commentary

- International arrivals at the Athens International Airport increased by 8.9% y-o-y in 2016, which is higher than forecasted by the airport at the beginning of 2016. Especially Q4 was particularly strong with double growth figures throughout the period September – December. The Athens hotel industry benefited and increased occupancy levels with 9% and room rates by 6% in Q4 compared to same quarter in 2015.

- The airport of Thessaloniki recorded during H1 2016 an increase of international arrivals of 4.0%, while the increase during H2 was 16.1% compared to 2015. Occupancy improved by just 3% during Q4, while room rates declined, mainly due to December. Overall, RevPAR improved 5.4% y-o-y in 2016.

- The resort hotels had a strong Q4 sourced by significant increases of international arrivals at main airports during Q4 2016 compared to same quarter last year: Dodecanese +26.7%, Crete +33.3%, Ionian Islands +38.7%, Cyclades +43.8% and Kalamata +46.0%, which shows that the tourism season is lengthening. Overall resort hotels recorded an increase of 9.6% y-o-y in 2016.

- Competitive destination Madrid had a difficult Q4 mainly due to the performance in October. Rome improved occupancy levels, while room rates slightly decreased in Q4. With respect to Cairo we should point out that the shown drop of RevPAR during Q4 is caused by conversion of room rates to Euro as the central bank of Egypt massively devaluated its currency in November. Occupancy levels at hotels in Cairo show significant double digit increases during Q4 2016.

Record international arrivals in 2016, but travel receipts declined

- On the basis of data of the Bank of Greece up to November 2016 we estimate that international tourist arrivals reached 24.7 million in 2016, an increase of 5% y-o-y, while travel receipts declined by 7%

y-o-y to a level of € 12.8 billion.

- That means that the average expenditure per trip dropped from € 583 in 2015 to € 516 in 2016, representing a decline of 11.5%. Main reasons of this drop are the shorter length of stay, lower average spending per tourist overall and increase of tourism from Balkan countries who are lower spenders compared to other European countries.

- The average spending per trip declined for major source countries in 2016: 13.4% y-o-y for France, 14.0% y-o-y for Germany, 19.7% y-o-y for the United Kingdom, 26.2% y-o-y for the USA and 10.7% y-o-y for travellers from Russia.

Domestic tourism market is recovering slowly

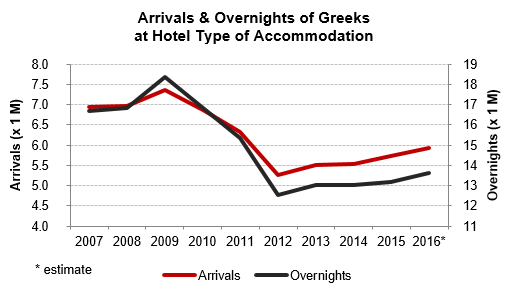

- Contrary to the record in international arrivals, the domestic tourism market is recovering at a very slow pace. As displayed in the graph, domestic arrivals and overnight stays declined sharply after its peak in 2009 to bottom levels in 2012. In those three years the hotel sector lost 2.1 million Greek arrivals and 5.9 million overnight stays.

- As from 2012 the domestic market is recovering. Compared to 2012 arrivals and overnight stays increased 13% and 9% respectively in 2016. However, compared to the peak of 2009 the hotel sector still has a gap of 1.4 million Greek arrivals and 4.7 million Greek overnight stays.

- Finally, the average length of stay of the Greeks at hotels decreased from 2.5 nights in 2009 to 2.3 nights in 2016

Latest developments

- After three rounds of failed auctions in 2016, Alpha Bank has lowered its starting price from € 47.8 million to € 36.5 million for the 5-star 314 room Athens Ledra Hotel. A new auction is currently planned.

- In December it was announced that Leisure Holding SA, part of the Lanitis Group in Cyprus, has signed a purchase agreement with London & Regional Group Trading registered in the UK for the purchase of 100% of the shares of Landa AXTE, who is the owner of the 5-star 318 room Amathus Beach hotel in Rhodes. Enterprise value has been determined at € 30.5 million, while debt to the banks amounts to approximately € 23.2 million.

- In November 2016 Sani - Ikos Group announced the acquisition of the 301-room Corfu Chandris and the 251-room Dassia Chandris from the Chandris Hotel & Resorts chain. Both hotels are currently of the 4 star category, but the units will be transformed into the 5-star Ikos Dassia resort with a capacity of 410 rooms. The total investment is estimated at € 110 million and the hotel will start operations in May 2018.

- In our newsletter of 2016 Q3 we have already reported on the former Kefalos Kos Club Mediterranee, which will start operations in spring 2019 as the 5 star Ikos Kefalos after an investment of around € 90 million. Ikos Resorts will then have 4 resorts in operation: 2 in Halkidiki, 1 in Corfu and 1 in Kos.

- Two years after the announcement that NCH Capital won the permission to develop an upscale hotel with residential units in Kassiopi, Corfu (see our newsletter of 2014 Q1), the privatization deal was finalised in December 2016 with the signing of the transaction. NCH paid € 23 million for the acquisition of the leasehold and will invest € 75 million for the development of the site.

- Finally, it is rumoured that Choice hotels is planning an entry in the Greek market and that Accor will finally establish its first hotel in Greece carrying its Ibis brand

Outlook

- Talks with bailout lenders remain at an impasse over the participation of the IMF in Greece’s 3rd bailout programme, which seems non-negotiable, and over demands for deeper cuts through the obligation to legislate a package of measures to address the potential deviation from the target of a primary surplus of 3.5% in the medium term beyond 2018. Furthermore, the adoption of many of the planned structural reforms will be crucial to boosting export performance and building a sustainable recovery. Without a return to growth, high levels of Greek debt may quickly become unsustainable again.

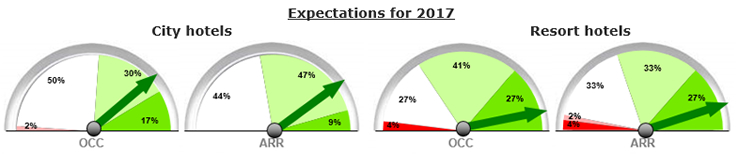

- Despite the lingering insecurity due to ongoing bailout negotiations and the instability in the region overall, hoteliers are very optimistic for 2017 according to the GBR Consulting barometer for 2017 with a majority expecting increases in occupancy levels and room rates in 2017 compared to last year.

- The city hoteliers expect to continue the positive trend of 2016. For the market overall, 47% is expecting improvements in occupancy levels of at least 2%, while 56% is expecting these growth levels for ADR.

- The projections of the resort sector are even more optimistic with 68% and 60% of hoteliers expecting improvements of at least 2% compared to last year for occupancy and room rates respectively.

Endnotes

1 The international arrivals statistics are based on SETE calculations compiling the data from 13 major airports of Greece, representing 95% of foreigners' arrivals by plane in Greece and 72% of total foreigners' arrivals. Thessaloniki airport does not distinguish between arrivals of Greeks and foreigners.

2 RevPAR : Revenue per Available Room; for Greek resorts, calculations are based on TRevPAR (i.e. Total RevPAR). |