Introduction

This newsletter provides a snapshot of the performance and outlook of the Greek hotel industry, within the broader context of the international hospitality industry as well as of Greek tourism and Greek socio-economic developments.

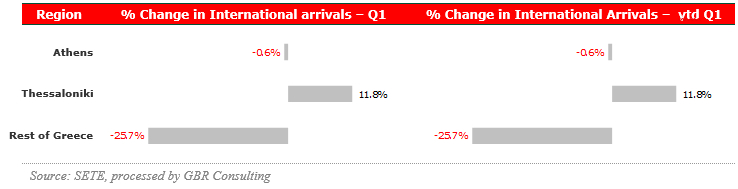

International arrivals1 at Greek airports, 2017 compared to 2016

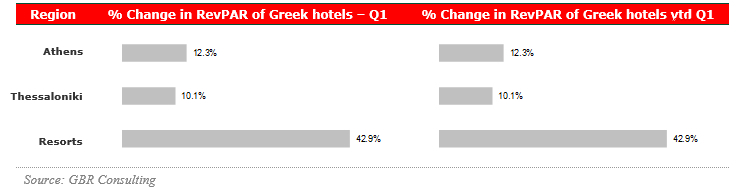

RevPAR2 in Greek hotels, 2017 compared to 2016

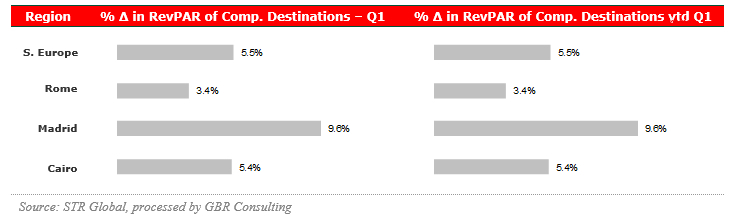

RevPAR in Competitive Destinations, 2017 compared to 2016

Commentary

- At the Athens International Airport total international arrivals declined in Q1 2017 with 0.6% y-o-y, mainly caused by the performance of the month of February, which recorded a drop of 7% y-o-y.

- Occupancy levels as well as room rates of Athenian hotels showed a positive trend, resulting in an improvement of RevPAR in Q1 2017 of 12.3% y-o-y.

- International arrivals at the airport of Thessaloniki increased significantly by 11.8% y-o-y during Q1 2017. February was particularly strong, which was reflected in the occupancy levels of the Thessaloniki hotel sector. Overall, RevPAR increased by 10.1% y-o-y in Q1 2017.

- Those resort hotels that were in operation during Q1 started the year well. However, most resort hotels are still closed.

- The hotel sector of competitive destination Madrid showed a good performance during the first quarter of 2017, especially in terms of room rates. Overall, RevPAR improved by 9.6% y-o-y in Q1 2017, while Rome improved by 3.4% y-o-y due to improved occupancy levels, but at a slightly lower ADR level compared to same quarter last year. Hotels in Cairo attracted much more tourists during Q1 2017 compared to same quarter last year resulting in improvements in RevPAR.

Greek tourism in 2017

- The Greek Tourism Confederation is optimistic for 2017 forecasting at least 26 million international tourists, representing an increase of 5% and significantly higher receipts, targeting at € 14.4 billion, an increase of 12.9% y-o-y. We assume that this increase is based on expected changes in the market mix.

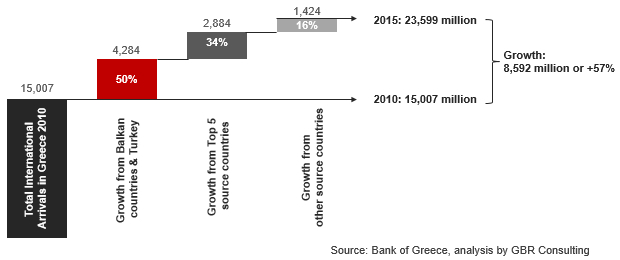

- As already reported in our Q3 and Q4 2016 newsletters, the declining travel receipts were partly caused by the increase of tourists from Balkan countries, who are overall low spenders on average. More specifically, 50% of the international tourism growth in the period 2010 – 2015 was sourced from Balkan countries and Turkey as displayed below.

Source of growth of arrivals 2010 – 2015 (x 1 M)

- In 2015 33% of all international arrivals came from Balkan countries (FYROM, Albania, Serbia & Montenegro, Bulgaria, Romania and Slovenia) and from Turkey.

- Data of the Bank of Greece for January and February 2017 showed declines in tourism arrivals and receipts, but in 2016 both months were representing just 4.0% of total international arrivals and 2.5% of total travel receipts and are therefore not representative for the course of the tourism sector in 2017.

- On an economic level business confidence and employment have both staged notable recoveries, which suggests Greece is past the nadir of its recession. Unemployment too, which peaked at nearly 28% in 2013, has since fallen by 5% points to 23.1%. But despite official forecasts for growth of 2.7% this year, a sustained and robust recovery remains elusive. This year will see another significant fiscal consolidation with tax rises and even though the Greek government reached a political agreement with the institutions at the Eurogroup in Malta at beginning of April, the second review still has not been finalised.

- Also the banks continue to struggle under high level of non-performing loans. NPLs in Greek tourism currently amounts to € 3.6 billion, of which € 1 billion is owed to banks by 5 major hotel companies, while € 600 million has already been rescheduled by Greek banks.

- In terms of tourism infrastructure, Fraport Greece has finally taken over the management of the 14 regional airports. Fraport will start infrastructure works after the summer, for which it entered a € 357 million deal with construction company Intrakat. Also at the end of April it was announced that a German led consortium will take over operation of Greece’s second-largest port for 34 years under a separate concession agreement.

- In the rankings of the Travel and Tourism Competitiveness Report 2017, made public in April, Greece jumped 7 places to the 24th position out of 136 countries in total. However, more work needs to be done to improve its business environment (103rd) with lower impediments to FDIs, lower taxation and enhanced efficiency of the legislative system.

Thessaloniki

- At the beginning of April GBR Consulting presented together with the Thessaloniki Hotel Association the results of the Tourist Satisfaction Survey & Performance of the Hotel Sector 2016.

- The research, conducted for the 6th time in a row, showed that the size of the Thessaloniki hotel sector has remained stable over the past 10 years and currently consists of 138 units. However, as demand increased, occupancy levels improved accordingly and reached the same level as cities like Dusseldorf and Cologne in Germany. The room rates did not follow the same trend and compared to European peers ADR levels remained the lowest after Bratislava.

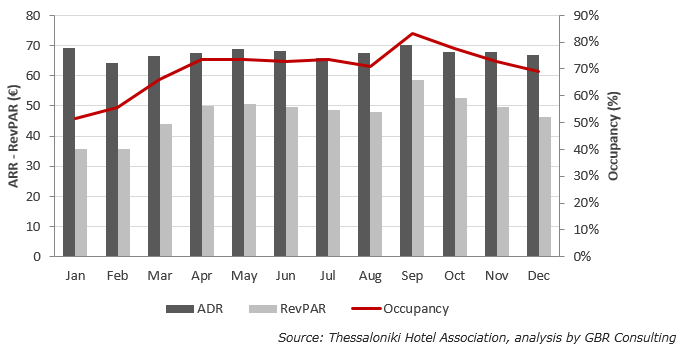

- In 2016 the lowest occupancy and room rate levels were recorded during the first quarter. Occupancy peaked in September. In terms of ADR the Thessaloniki hotel sector did not show a particular pattern in 2016. ADR fluctuated between € 64 and € 70.

Performance of the Thessaloniki hotel sector in 2016

- Tourist satisfaction levels remain very high with an overall satisfaction rate of 8.3 out of 10 of the leisure travellers and 8.1 out of 10 of the business travellers. Entertainment, the inhabitants and the culture of Thessaloniki continue to be the most appreciated aspects of the city.

- Finally, it is very interesting that 69% of the foreign leisure travellers visited Thessaloniki only, while 31% also included other destinations in their trip including Central Macedonia. This indicates that there are substantial opportunities for Central Macedonia as a destination with the city of Thessaloniki, Halkidiki, Vergina, Pella, Olympos, Dion and Mount Athos as the main ingredients of the rich tourism product of the region.

Announced deals in the Greek hospitality sector

- In February it was announced that Zeus International has reached a lease agreement of the Poseidon Resort in Loutraki, a 5 star unit of the Argyrou family located at a one hour drive from Athens. The indebted hotel will be rebranded as the 108-room Wyndham Loutraki Poseidon hotel and the 207-room Ramada Loutraki Poseidon. Ramada is a brand of Wyndham Worldwide.

- Zeus International, as part of a wider development plan with the Wyndham Hotel Group signed deals in March with 2 hotels of the Xenotel Hotel Group in Attiki: the 346-room Mare Nostrum in Vravona and the 129-room Aqua Marina in Nea Makri. The hotels will be rebranded as the Ramada Plaza Attica Riviera and the Wyndham Garden Attica Riviera and will be in operation as such from 2018.

- Accor, which currently has the Novotel and Sofitel in Athens in their portfolio, announced in March that it will expand with an Ibis Styles hotel in Heraklion, Crete. The 72-room Ibis Styles Heraklion Central Hotel will be constructed by Polis H.M. S.A with a budget of € 15 million. Furthermore, Accor is planning for a first Ibis hotel in Athens and a Novotel in Piraeus.

- In February Eurobank confirmed that out of 5 bids the preferred buyer of the 700-room Capsis hotel is Nikos Koutras, owner of two major resorts on the island of Kos. However, the deal, which involves an amount of € 30 million has not been finalised.

Latest developments in Athens

- The fourth auction of the 314-room Athens Ledra at Syngrou Avenue and the first auction of the 208- room La Mirage hotel at Omonia Sq failed despite expressed interest from local and foreign investors. In both cases there were no bids.

- According to press reports there is strong interest from hotel enterprises in the tender for a long-term lease of a property located at Panepistimio St, near Syntagma. The 9-floor property of 13,244 sqm used to house the Agrotiki Bank and many years ago it was home to the King’s Palace hotel.

- In 2017 two new boutique hotels started operations. At Syngrou Avenue the 13-room NHL Fix hotel opened as the first hotel of a new chain, Neighborhood Lifestyle Hotels, which is planning to open another 3 units in Athens by the end of 2018. The second unit, the 18-room NLH Gerani will be opened this year near Omonia Sq. Furthermore, the 25-room Lozenge Hotel re-opened in Kolonaki, which was formerly known as the Lycabettus Hotel.

- Various other new boutique hotels are planned in Plaka at the former Aiolos hotel (1836), in Mitropoleos St (Grecotel), near the Acropolis (Coco-mat), in Kolonaki and at a building at Filelinon St

Latest developments at resort locations

- In Chalkidiki the Tor Hotel Group, of the Tornivoukas family, has just opened the 5 star Eagles Villas on a plot next to the 5 star Eagles Palace resort of the group on the Mount Athos Peninsula. Total investment of the 40 villas amounts € 11.5 million. The Tor Hotel Group also operates the Excelsior and the City Hotel in Thessaloniki.

At the end of June Sani Group will open the new 5-star 136 room Sani Dunes within Sani Resort. The total investment amounts € 24.2 million.

Finally, plans have been released for the construction of the 92-room 5 star Blue Lagoon Palace hotel with a budget of € 12 million, next to the 5 star Blue Lagoon Princess, operated by the Blue Lagoon Group.

- In Crete, adjacent to the 5 star Nana Beach hotel, Karatzis S.A. has started construction of the new 120-room Nana Imperial in Hersonissos. Almost all suites and villas will have private pools. The hotel will start operations in April 2018. In addition the mother company of Karatzis S.A. is planning for another 350 rooms resort at a coastal property of 140 stremma in Ierapetras, Lasithi.

The Hersonissos Group of Hotels, which owns and operates 7 hotels in the area of Hersonissos will construct the new 150-rooom 5 star Abaton Resort with an estimated budget of € 25 – 30 million

- In Rhodes plans have been announced for the development of 187-room 5 star hotel by Ammos SA in the area of Lindos.

- Finally, in Zakynthos the new 5 star 93-room adults only Lesante Blu Exclusive Beach Resort will open in May at a beachfront plot in Tragaki, Zakynthos.

Endnotes

1 The international arrivals statistics are based on SETE calculations compiling the data from 13 major airports of Greece, representing 95% of foreigners' arrivals by plane in Greece and 72% of total foreigners' arrivals. Thessaloniki airport does not distinguish between arrivals of Greeks and foreigners.

2 RevPAR : Revenue per Available Room; for Greek resorts, calculations are based on TRevPAR (i.e. Total RevPAR). |