Introduction

This newsletter provides a snapshot of the performance and outlook of the Greek hotel industry, within the broader context of the international hospitality industry as well as of Greek tourism and Greek socio-economic developments.

Performance

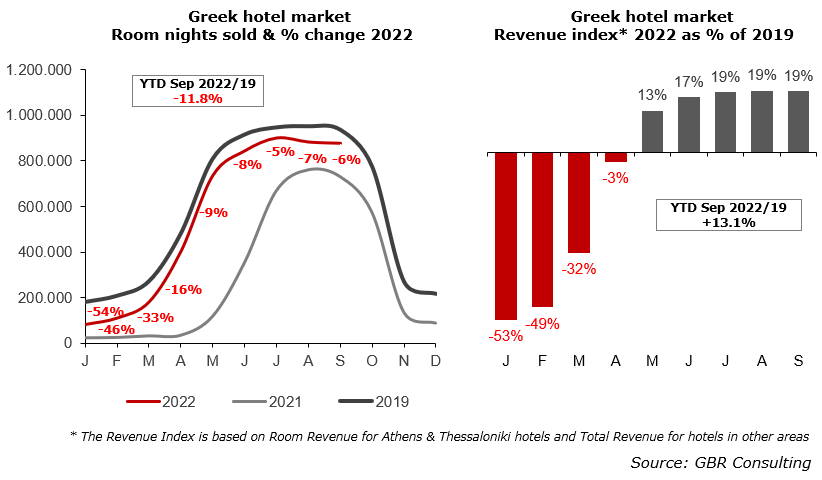

- Based on the monthly hotel performance survey conducted by GBR Consulting on behalf of the Hellenic Hotel Federation, the Greek hotel sector showed during Q3 2022 a decline of the number of room nights of 5 – 7%, while the revenue index showed an increase of 19% compared to the same period of 2019.

YTD September 2022/2019 room nights declined 11.8% while revenues increased 13.1%.

- The Bank of Greece reported up to August 2022 an increase of 10.6% of the average spent per trip from € 591 in 2019 to € 654 in 2022. The total number of international visitors declined 12.4% YTD August 2022/2019, while for 2022 as a whole it is expected that total travel receipts will reach 2019 levels.

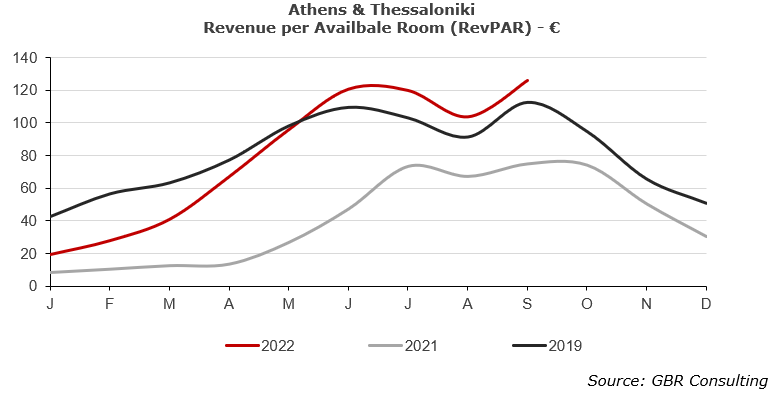

- Data of Athens and Thessaloniki, collected on behalf of the Attica-Athens and Thessaloniki Hotel Associations, shows that occupancy levels up to September 2022 were 14.7% lower than same period of 2019, while ADR increased 14.4% YTD September 2022/2019. As a result RevPAR decreased by 2.5%. During the months of June, July, August and September of 2022 RevPAR surpassed the levels of 2019 due to higher room rates as occupancy levels were lower.

- A similar trend is noted for city hotels outside Athens and Thessaloniki, where occupancy levels with the exception of May were lower so far than the months of 2019. Also, total revenue was significantly lower in 2022 than 2019 during the period January – March, but recorded higher levels in May and June.

International arrivals at airports on par with 2019 levels, domestic arrivals declined

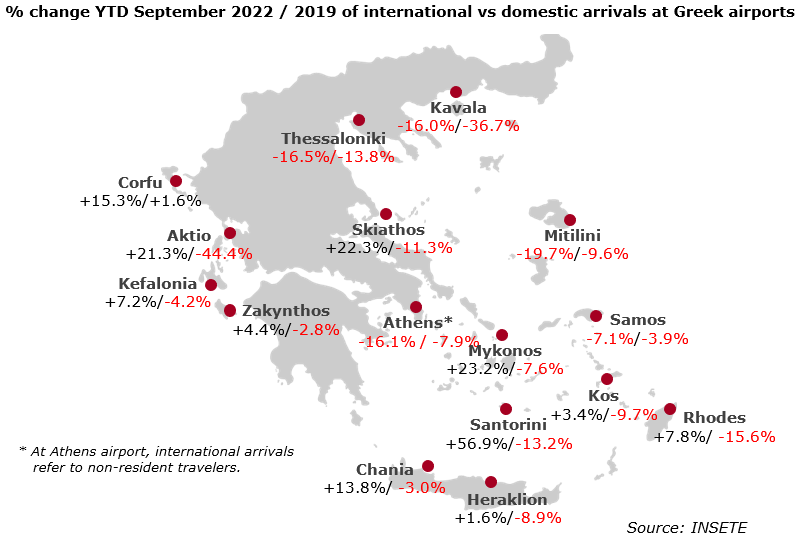

- As mentioned above, international arrivals declined and reached up to August 2022 a level of 88% of the level of 2019. This is mainly caused by a significant decrease of 35% YTD September 2022 / 2019 of road arrivals according to data released by INSETE. In this respect it should be noted that in 2019 30% of a total of 31.3 million arrivals were sourced from Balkan countries (Bulgaria, Romania, Serbia / Montenegro, North Macedonia, Albania & Slovenia) and Turkey.

- International arrivals at the main airports of Greece up to September 2022 are on par with 2019 levels, but as shown below there are significant differences per region. Greece’s largest airports of Athens and Thessaloniki recorded a decline of 16.1% and 16.5% respectively YTD September 2022/2019, while the largest international airports on the islands recorded increases in international passenger arrivals: Rhodes +7.8%, Kos +3.4%, Heraklion +1.6%, Chania +13.8% and Corfu +15.3%.

- Domestic arrivals at the airports declined 9.3% YTD September 2022/2019.

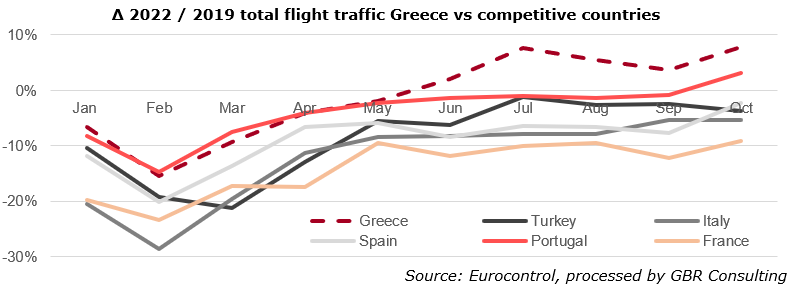

- Total arrivals (international & domestic) at Greek airports declined 2.5% YTD September 2022/2019, while according to Eurocontrol the number of flights increased 2.0% YTD October 2022/2019, which means that the load factor, the occupancy of airplane seats, has decreased.

Headwinds will limit Greek economy’s medium term prospects

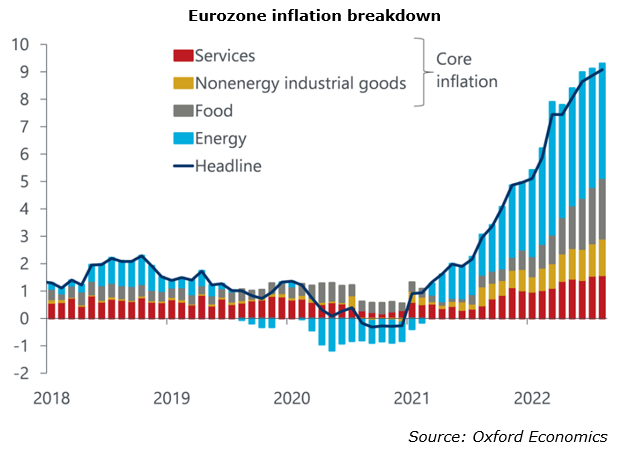

- According to Eurostat estimates, inflation in the Eurozone set a new record in October as the price index increased by 10.7% y-o-y. High inflation will weight on demand, dragging down growth and pushing the Eurozone into a recession this winter, mainly driven by negative industrial dynamics according to Oxford Economics. As shown in the graph, the rise in prices is driven by energy and food, followed by services and nonenergy industrial goods. Further aggressive tightening is expected by the ECB with substantial rate hikes in October and December.

- Eurostat inflation estimates for Greece show a drop from 12.1% in September 2022 to 9.8% in October 2022. Oxford Economics expects that prices will remain higher for a longer period. In combination with higher interest rates this will negatively affect disposable income. The energy crisis is deteriorating the outlook of Greece’s industrial sector. For 2023 a 0.2% contraction of GDP is expected for Greece (-0.1% for the Eurozone) but with risks tilted to the downside as the energy crisis could worsen unexpectedly and the war could last longer than expected. Moreover, an escalation in rhetoric from high level officials in Turkey could fuel tension in the Mediterranean region.

- The effect for the tourism sector and next season is uncertain. High inflation with high energy costs, lower disposable incomes, lower confidence, higher jet fuel prices and expected higher air fares will have an impact. Middle and lower income households will be hit hardest. In addition, the hospitality sector has to deal with staff shortages, while maintaining high standards and high quality of services. The satisfaction index for Greece of ReviewPro - the GRI Index - published by INSETE, declined for each of the months of July, August and September comparing 2022 with 2019.

Main transactions

- In October 2022 it was announced that the 4-star Elatos Resort & Health Club was sold by Elatos Investment Ltd, an interest of the Eletson shipping company of the Kertsikov, Hatzielethriadis and Karastami families to Athanasios Laskaridis, the main shareholder of the Lampsa group. Elatos Resort offers 40 wooden chalets located in the area of Eptalofos on the northwest of Mount Parnassos at a distance of 35 minutes to the Parnassos Ski Center (Kelaria) and to Arachova. The property will be transformed into a luxury mountain resort with an emphasis on wellness attracting guests throughout the year. No further transaction details were revealed. The resort is expected to re-open in 2024.

- Intrakat announced in October 2022 the acquisition of the Apanema Resort in Mykonos for an amount of € 10.6 million. The property, located 900m from Mykonos town, currently has 17 spacious rooms, but will be fully renovated and return to the market as a high-end boutique hotel. Intrakat also has in its boutique hotel portfolio Branco Mykonos, the Met34 and the Milos hotel (opened this year) in Athens. In Mykonos Intrakat is also developing a residential complex of 200 beds in Ano Mera.

- Sani/Ikos Group (SIG) and GIC, global institutional investor, announced in September 2022 that they have entered into a strategic partnership under which GIC will become the leading shareholder. The transaction values the Sani/Ikos Group at € 2.3 billion. The transaction is expected to close in the 4th quarter of 2022, subject to customary regulatory approval.

Since its creation in 2015 SIG has expanded its asset base and scale by a factor of four with the backing of blue-chip investors including funds managed by Oaktree Capital Management L.P., funds managed by Goldman Sachs Asset Management, Moonstone, Florac and Hermes GPE who will be selling their stakes to GIC as part of this transaction. Andreas Andreadis and Mathieu Guillemin will continue to manage SIG as CEOs and Co-Managing Partners, while Stavros Andreadis will become Honorary Chairman of the Group. All also remain significant shareholders.

- Although reported in the media as from February this year, we understand that a deal between Grigoriadis Family and Goldman Sachs Asset Management has been completed. The deal concerns 3 hotels of the Ghotel Group located near the town of Kallithea, Kassandra, Halkidiki on a plot of land of about 142 stremma: the

4-star Pallini Beach with 485 rooms & bungalows, the 4-star Athos Palace Hotel with 413 rooms and the 5-star Theophano Imperial Palace offering 151 rooms. The total current room count of the deal is 1,049 rooms. In the coming years it is expected that the property will be repositioned.

Other hotels of the Ghotels Group are the 5-star Simandro Beach (367 rooms), the 3-star Macedonian Sun (147 rooms), both located in Halkidiki and the 3-star Panormo Beach in Rethymno, Crete (43 rooms).

- Beginning of August 2022 it was announced that the 5-star 401-room Sheraton hotel in Rhodes was sold by Lampsa SA to Azora European Hotel & Lodging F.C.R for an amount of € 43.8 million (€ 109,000 per room). Lampsa SA has a portfolio consisting of the

5-star hotels Grand Bretagne, King George and Athens Capital in Athens and the Hyatt Regency and the Mercure Excelsior in Belgrade, Serbia. For Madrid-based Azora it is the first hotel acquisition in Greece.

- In June the Grande Mare Hotel was finally sold in an auction for € 5.89 million after numerous attempts. We did not recorded the transaction in our Q2 2022 newsletter. The property is located in Benitses, 10 km south of Corfu Town in front of the 5-star Angsana Corfu. The Grande Mare does not have direct access to the beach.

- Finally, end of October Mitsis Hotels Group announced that it expands its operation with a 20-year management agreement with Happy Holidays SA for a new 5-star resort located near the village of Sarti, Sithonia, Halkidiki. The resort will consist of a 5-star boutique hotel offering 52 rooms, conference & wellness center, a 5-star all-suites hotel offering 98 rooms, a thalassotherapy center, F&B and retail square and a tourist boat shelter with a capacity of 20 berths.

Mitsis Hotels Group will contribute to the pre-planning phase of the project which will include the definition of the brand concept, business planning, performance management as well as the propositions of technical, design and construction functions.

|