Introduction

This newsletter provides a snapshot of the performance and outlook of the Greek hotel industry, within the broader context of the international hospitality industry as well as of Greek tourism and Greek socio-economic developments.

The year 2023 in review

Commentary

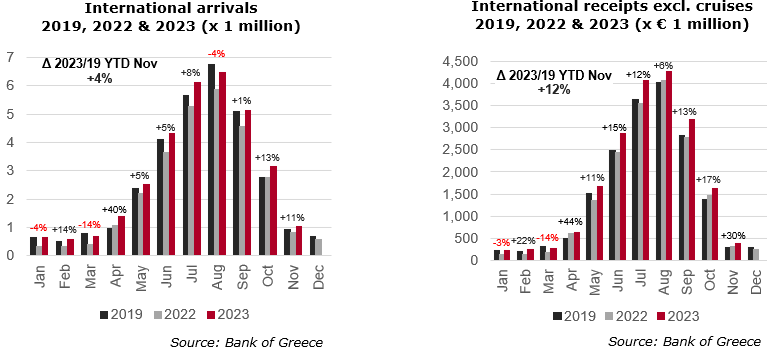

- Greek tourism registered in 2023 a record year surpassing the levels of 2019. YTD Nov 2023/19 international arrivals increased by 4% reaching 32 million, while international receipts increased by 12% to € 19.4 billion excluding receipts from cruises. Cruise receipts reached € 699 million YTD Nov 2023, +40% compared to 2019, so total travel receipts surpassed for the first time the level of € 20 billion.

- It is interesting to note that international arrivals in August 2023 declined 4% compared to 2019 (see graph above), while all other months of the main season running from April – October recorded increases. The hot temperatures and wildfires, particularly the one in Rhodes that destroyed 14.5% of the total surface area of the island, could have contributed to the decline in August.

- Among the major source markets, the UK outperformed with an increase YTD Nov 2023/19 of 31% in international arrivals and 30% in terms of travel receipts. The number of US travellers increased from 1.1 million in 2019 to 1.4 million in 2023 up to November, an increase of 19%.

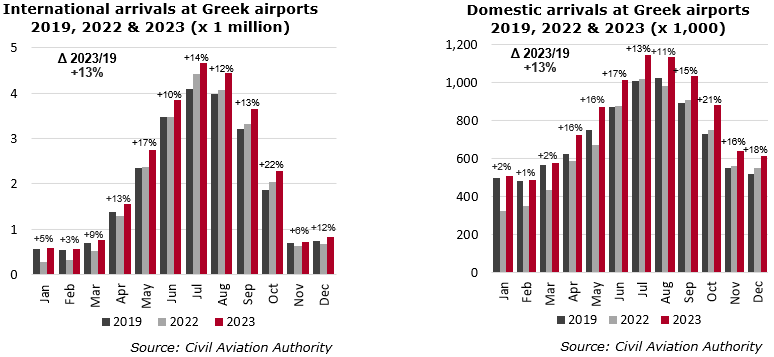

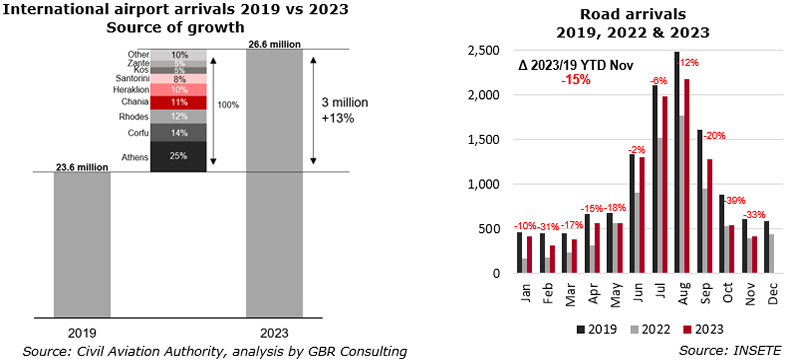

- The growth in international arrivals is attributed to the increase of 13% of international passengers at the Greek airports as road arrivals declined by 15% (YTD Nov) comparing 2023 with 2019. International airport arrivals increased from 23.6 million in 2019 to 26.6 million in 2023. The Athens International airport alone is responsible for 25% of this growth of 3 million, followed by Corfu, Rhodes, Chania, Heraklion, Santorini, Kos and Zakynthos as the main contributors. These 8 airports were responsible for 90% of the registered growth.

- The Athens International Airport, which recorded 9.6 million international arrivals including Greeks arriving from abroad, launched on January 24th, 2024 together with the Hellenic Republic Development Fund (HRADF) a prospectus for the biggest Initial public offering (IPO) after the 2010 – 2018 debt crisis for a 30% stake in Athens International Airport by selling 90 million shares at a set price range of € 7.0 – € 8.2, implying a market value of € 2.1 to 2.5 billion. The listing on the Athens Stock Exchange is expected to take place on February 7th, 2024. It is expected that the IPO could generate up to € 1.2 billion for the Greek state. The Athens International Airport has agreed to pay shareholders a € 685 million dividend in connection with the IPO including government entities.

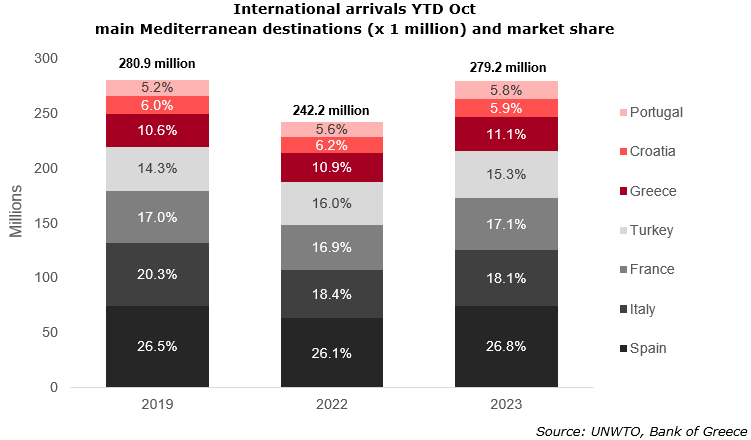

- Compared to main European peers, Greece gained market share in 2023 compared to 2019, just like Portugal and Turkey based on international arrivals up to October. International arrivals in Italy YTD Oct 2023/19 declined by 11.4% resulting in a significant loss of market share, while the market share of Croatia dropped slightly due a decline of international arrivals of 2.6% YTD Oct 2023/19.

- In total these countries attracted up to October 279.2 million international arrivals, representing a decline of 0.6% compared to same period in 2019. Portugal was the best performer with an increase of 11.0% YTD Oct 2023/19, followed by Turkey with 6.3% and Greece with 4.1%.

Greek hotel sector performance

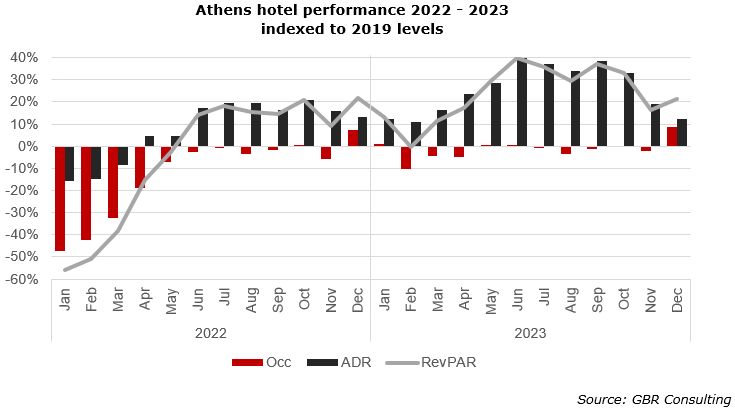

- The recovery of occupancy levels at Athenian hotels stalled in 2023 with demand for Athens at record levels. Room rates, however, increased significantly as from June 2022. YTD Dec 2023/19 occupancy declined 1.5%, while ADR improved by 29% and as a result RevPAR increased by 27%.

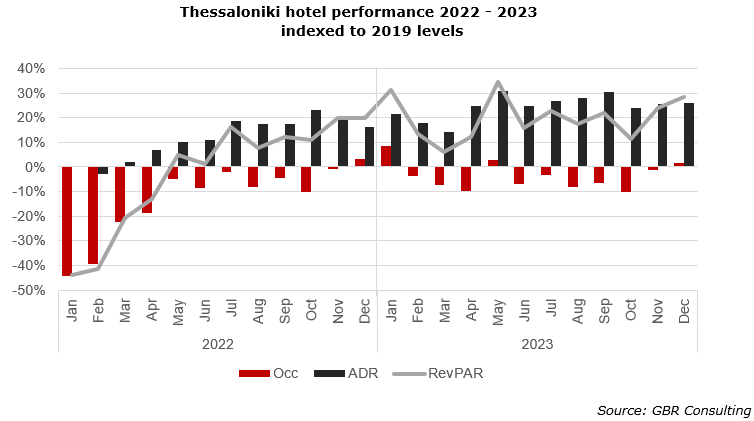

- At the hotels in Thessaloniki, occupancy remained overall below the levels of 2019, but ADR significantly improved. YTD Dec 2023/19 occupancy declined 4.2%, while ADR improved by 25%. RevPAR, therefore, recorded an increase of 19.7% comparing 2023 with 2019.

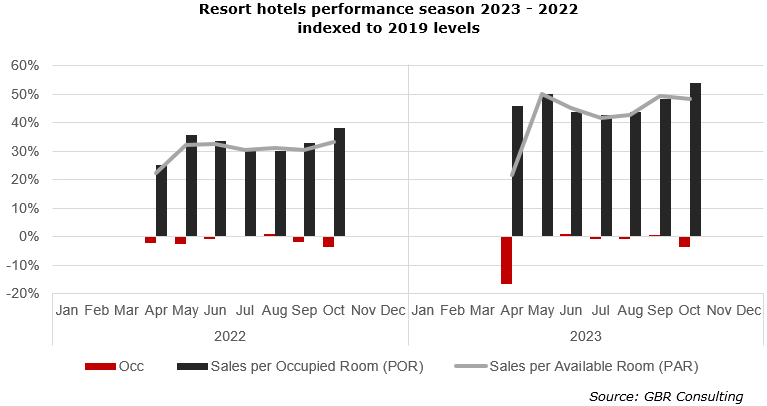

- Resort hotels during the season of April – October registered slightly lower occupancy levels in 2023 and 2022 compared to 2019. Only April 2023 saw a significant decline due to an increase of available rooms, but with same demand levels as a year earlier. YTD Dec 2023/19 occupancy declined 1.8%, but the Total Sales per Occupied Room increased significantly by 45%. Consequently, Total Sales per Available Room improved by 42%.

Outlook & challenges

- The outlook for the tourist season of 2024 is positive. The year of 2023 has shown that Greek tourism was not affected by high inflation, lower disposable incomes, global economic slowdown and geopolitical conflicts. As indicated above, natural disasters seems to have an impact and at a local level – see the Rhodes wildfires – this is a fact.

- It is noted that in December 2023 the Greek Government passed a new law to replace the stayover tax with a climate crisis resilience fee. The charges have been increased significantly for the season running from March – October. The below fees are per room per night:

- Last season Greece experience numerous natural disasters. The revenue generated from the above charges will be allocated to establish an emergency fund dedicated to addressing natural disasters.

- With the record receipts of 2023, Greece’s reliance on the tourism sector has increased further and thus its vulnerability. Major challenges such as climate change and demographic shifts will have a major impact on the Greek tourism industry in the long run and therefore both issues require a long term vision far beyond a political term of 4 years.

- At an Economist conference of January 2024, solutions were sought for the expected declining population in Greece as the birth rate is much lower than the mortality rate resulting in an aging population and a shrinking workforce.

- A diminishing active workforce carries significant consequences, and addressing this challenge requires a comprehensive approach that takes into account various factors:

- Education: invest in education and skill development to ensure a competent and adaptable workforce

- Increase fertility rates: mitigate factors limiting child birth, such as financial constraints, by enhancing disposable income and providing support systems

- Increase participation of women in the workforce: provide child care solutions, education, remote work options, address wage gaps and improve work-life balance and change of culture

- Retain older workers: implement health care programs to keep them healthy, enable them to work longer as life expectancy is increasing, ensure their skills remain up-to-date, alleviating pressure on social systems

- Prevent Brain Drain and encourage Brain Gain: create measures to retain local talent and attract skilled professionals

- Immigration: strategically utilize immigration to supplement the workforce, contributing to economic growth and diversity

- Leverage technology including artificial intelligence: embrace technological advancements, including artificial intelligence, to enhance productivity and efficiency in various sectors

Transactions

- In January 2024 it was announced that H Hotels Collection, Hatzilazarou Group, acquired the 5-star Rhodes Bay Hotel & Spa including Elite Suites Rhodes Bay with a total room count of 357 from the British London & Regional Group, which acquired the property in 2017. L+R also owns the 4-star Titania in Athens and is participating in a joint venture for the development of a 5-star mixed use resort in the area of Kalo Livadi in Mykonos. With the acquisition, H Hotels has a total of 7 hotels and more than 2,300 rooms in Rhodes making it the largest local chain in Greece.

- At the beginning of January 2024 it was announced that Prodea sold the 207-room Dolce Milan Malpensa in Italy and the 5-star 74-room Lazart Hotel in Thessaloniki to Zeus International. The property was acquired in 2018 by NBG PANGAEA REIC (today known as Prodea Investments) for € 7 million. Zeus International leased the property as from 2017. With these deals, 9 out of 20 hotels in the portfolio of Zeus International are owned.

Furthermore, it was announced that MVH Mediterranean Hospitaly Venture Plc sold the remaining 50% stake in Aphrodite Hills Resort Limited to W.R.A. Consultants (WRA), an interest of the Nicolaides brothers, who also run Atlantica Hotels. MVH acquired in November 2021 100% of the shares of Aphrodite Hills Resort Limited and sold in September 2022 the first 50% to WRA.

MVH was owned by Prodea Real Estate Investment SA (25%), Flowpulse Limited (20%) and Ascetico Limited (55%), which is owned by Yoda Plc, an interest of Ioannis Papalekas (Globalworth). In December 2023 it was announced that Prodea acquired the 55% from Ascetico Limited, bringing Prodea’s share of MVH to 80%. In January 2024 it was reported that the € 254 million transaction was completed.

After the above mentioned deals MVH – 80% Prodea and 20% Flowpulse - owns in terms of hotels:

- Cyprus: the 5-star Parklane – Luxury Collection in Limassol, the 5-star Landmark Nicosia, Autograph Collection (the former Hilton) planned for opening at the end of 2024 and a residential and office tower on the same property.

- Greece: the 5-star Nikki Beach in Port Heli and the 242-room Porto Paros in Greece. In December 2021 the Greek subsidiary of MVH entered into pre-agreements for its acquisition (media reported

€ 57 million), but we understand that the transaction has not yet been completed. The 4-star hotel will redeveloped into a luxury resort.

Prodea owns in terms of hospitality assets in Greece the Moxy Patra, the Moxy Athens City through Rinacita SA, Ergon House in Athens and 49% of V Tourism SA, owner of the White Coast Pool Suites in Milos, which was purchased in December 2022. The remaining 51% belongs to Invel, which controls Prodea.

Finally, in January 2024 it was made public that Yoda PLC acquired a 5.22% stake in Prodea.

- At the beginning of January 2024 Intracom Holdings announced the acquisition of a 71.31% stake for an amount of € 4.3 million of the company Simou Brothers, which owns the 4-star 50-room Koufonisia Hotel located on Koufounisia island in the Cyclades. The loans of Simou Brothers were part of the Tethys deal, which we reported in Q1 2023.

- Beginning November 2022 Blackstone announced that it has agreed to sell a 35% stake in Spanish group Hotel Investment Partners (HIP) to GIC. The financial times reported that the deal values HIP at more than € 4 billion. HIP currently owns 73 hotels offering 21,831 rooms with most of the properties located in the Canary Islands (45%), but also in the Peninsular Coast and the Balearic Islands (38%) and in Italy & Greece (17%). The portfolio in Greece consists of 7 properties offering 1,708 rooms:

- In Crete, the 5-star Creta Princess Aquapark & Spa (418 rooms) and the 5-star Domes Aulus Elounda (182 rooms)

- In Corfu, the 5-star Dreams Corfu Resort & Spa (337 rooms) and the 5-star Domes of Corfu (236 rooms)

- In Zakynthos, the 5-star Domes Aulus Zante (197 rooms) and the 4-star AluaSoul Zakynthos (156 rooms)

- In Halkidiki, the 4-star Domes Noruz Kassandra (182 rooms)

Finally, in January 2024 it was made public that Yoda PLC acquired a 5.22% stake in Prodea.

It is noted that in 2022 GIC became the largest shareholder in the Sani / Ikos Group in a transaction that valued international group of Greek origin at € 2.3 billion.

|