Hospitality Newsletter

Latest trends of the Greek hospitality sector

Explore Newsletters

The GBR Consulting Hospitality Newsletters provide a snapshot of the performance and outlook of the Greek hotel industry, within the broader context of the international hospitality industry as well as of Greek tourism and Greek socio-economic developments.

Greek Hospitality Industry Performance - 1st Quarter 2026

Stagflation and the consequences for the tourism sector

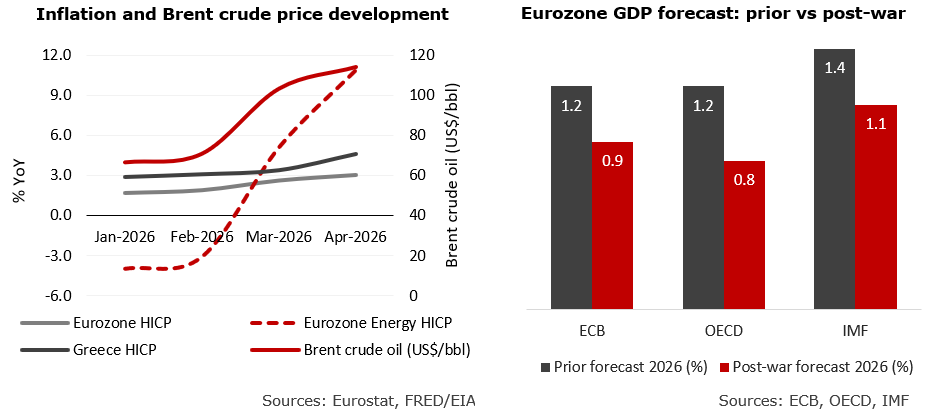

The escalation of the Iran conflict from 28 February 2026 has created an energy shock with implications for inflation, growth expectations, aviation costs and consumer confidence. The subsequent closure of the Strait of Hormuz sharply tightened global energy markets, with Brent crude rising above $ 120 per barrel. Eurozone headline inflation rose back to 3.0% in April, while energy inflation reached double digits, creating a stagflationary risk environment: inflation is re-accelerating at the same time as growth expectations are being revised down. This is already reflected in lower 2026 GDP forecasts by major institutions, including the ECB, OECD and IMF, as shown in the chart. The macroeconomic setting therefore leaves central banks with a more difficult trade-off between containing inflation and supporting demand.

For travel and hospitality, this is a more complex risk than a conventional downturn. In a recession, demand weakens but some costs also ease. In the current environment, demand may remain present while costs rise: energy, food and beverage inputs, logistics, insurance and financing costs are all under pressure, while consumers face higher airfares and reduced discretionary income. Airlines are particularly exposed because fuel is a direct operating cost, and higher jet-fuel prices can affect fares, route profitability and capacity decisions even where underlying travel demand remains resilient. The available evidence so far does not point to a collapse in tourism demand, but rather to a more cautious, more price-sensitive and more last-minute booking environment.

Greece: demand support, but weaker visibility and higher operating pressure

Greece enters the 2026 summer season in an ambiguous position: more favourable than many feared in early March, but more fragile than headline air-capacity numbers alone suggest. Southern Europe may benefit from some demand redirection away from destinations perceived as more exposed to the conflict. However, scheduled capacity does not automatically translate into realised demand, strong load factors or hotel profitability. Available market feedback suggests weaker booking conversion than at the same point last year, booking windows have shortened, and consumers are reassessing travel decisions in light of fares, inflation and geopolitical uncertainty.

The German market, historically one of Greece’s more price-sensitive major source markets, has become more cautious after the escalation, while the UK market appears more resilient, albeit with greater last-minute behaviour. At the same time, Greece faces the same margin-compression dynamic affecting Mediterranean hospitality more broadly: domestic inflation, at 4.6% in April, is above the Eurozone average, energy costs are feeding into electricity, cooling, food and logistics, and persistent labour shortages are adding wage and service-delivery pressure. A possible scenario for 2026 is therefore one of resilient headline arrivals combined with genuine pressure on operating margins. The key issue is not only whether demand materialises, but whether it converts into margins that justify current pricing, investment and transaction expectations.

Hotel sector performance

According to Bank of Greece data, inbound tourism started 2026 on a strong footing. During January–February, international arrivals reached 2.13 million, compared with 1.54 million in the same period of 2025, representing an increase of 38.5%. Growth was positive in both months, with arrivals up 33% in January and 45% in February.

Travel receipts excluding cruises increased even more strongly, reaching € 994 million in the first two months of 2026, compared with € 578 million in January–February 2025, an increase of 72%. Receipts rose by 59% in January and 86% in February, significantly outpacing the growth in arrivals.

Athens

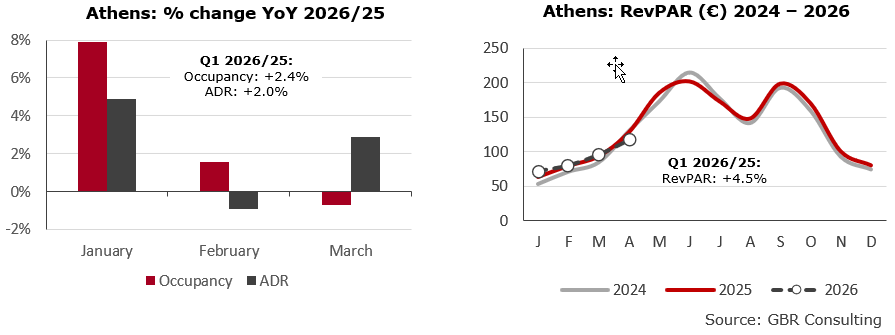

At the Athens airport, significant increases were recorded during January and February 2026 for both international and domestic traffic compared to a year earlier, while growth slowed in March. This performance was reflected in the KPIs of the Athens hotel sector.

During Q1 2026 occupancy and ADR improved by 2.4% and 2.0% respectively, resulting in a 4.5% increase in RevPAR compared with the same quarter last year.

The improvement is a continuation of the trend set last year, which showed a particularly strong winter performance. RevPAR improved by 13.5% in Q1 2025/24. By contrast, during April–October 2025 occupancy declined by 1.2%, although ADR still improved by 2.7%. This indicates that Athens is making progress in extending demand into the winter period.

However, in March 2026 we noted extreme performance differences between hotels, where some hoteliers registered very high demand improvements compared to last year, while others recorded significant declines.

Thessaloniki

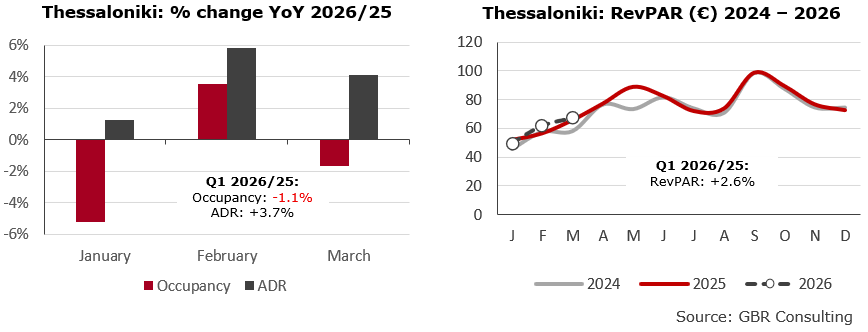

Thessaloniki’s hotel market recorded a modestly positive start to 2026, supported primarily by rate growth rather than stronger demand. In Q1 2026, occupancy stood slightly below last year’s level, down by 1.1% compared with Q1 2025, despite remaining 5.0% above Q1 2024. The monthly pattern was mixed: February showed a 3.6% year-on-year improvement, while January and March declined by 5.2% and 1.7%, respectively.

January’s softer occupancy may have been partly affected by external disruption, including farmer protests and road blockades that complicated domestic and cross-border travel.

ADR performance was stronger and more consistent. Average daily rate increased by 3.7% year-on-year in Q1 2026, following growth in all three months: +1.3% in January, +5.8% in February and +4.1% in March. ADR also exceeded the € 100 threshold in January and March, indicating that the market was able to maintain pricing power despite slightly softer occupancy.

As a result, RevPAR reached € 60 in Q1 2026, up by 2.6% compared with Q1 2025 and 10.6% above Q1 2024.

Nafplio: a high-satisfaction destination with room to grow hotel demand

Greek tourism remains highly concentrated in the country’s main tourism poles. In 2025, five out of Greece’s 13 regions — South Aegean, Attica, Crete, Ionian Islands and Central Macedonia — accounted for around 90% of travel receipts, 88% of overnight stays and 83% of visits, while representing 67% of hotels and 79% of hotel rooms. The remaining eight regions, including the Peloponnese, offer a diverse and authentic tourism product, with nearly 3,300 hotels and 95,000 hotel rooms, or an average of only 29 rooms per hotel.

Nafplio is one of these destinations in the Peloponnese. GBR’s visitor profile and satisfaction survey, conducted on behalf of the Municipality of Nafplio and based on 830 questionnaires collected during the April–November 2025 visitor season, confirms that Nafplio is attractive, accessible and distinctive, but still faces the challenge of converting its strong visitor appeal into higher accommodation demand

Nafplio combines a historic centre of national significance — reflecting its role as the first capital of modern Greece — with important cultural assets, proximity to Athens, gastronomy, coastal scenery and a high-quality visitor experience. The destination is primarily leisure-driven, with 83% of respondents visiting for leisure purposes. Archaeological and cultural interest, the character of the city and gastronomy are among the main reasons for choosing Nafplio, confirming its position as a cultural short-break and experience-led destination.

The demand base is relatively balanced between domestic and international visitors, at approximately 50–50. Among international visitors, the main source markets include the USA, France, Germany, Belgium, Italy and the Netherlands. The majority of visitors are aged between 36 and 70, couples represent the dominant travel group, and 61% visited Nafplio for the first time. The most visited attractions are the Palamidi fortress, the Bourtzi Castle and the Archaeological Museum. Average daily expenditure reached € 76 per person, with restaurants, cafés, bars and snacks representing the largest spending category.

Visitor satisfaction is particularly strong. In the survey, 67% of visitors stated that their experience was better or much better than expected, while 98% would recommend Nafplio to others and 92% would visit again. The overall rating reached 8.4 out of 10. These results suggest that the core product is well received once visitors arrive.

The Municipality of Nafplio has 55 hotels, 73% of which are in the 3- and 4-star categories, offering approximately 1,860 rooms. In addition, the short-term rental market becomes particularly active during the summer period, with more than 500 active units, while 56% of listings are available for 271–365 days per year.

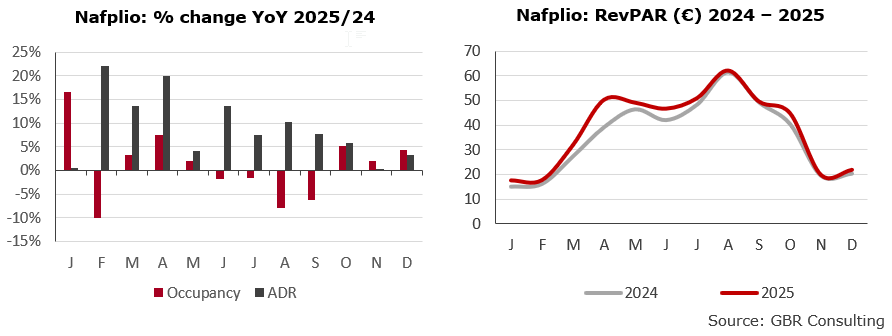

Hotel performance indicates that the destination has not yet fully converted its positive visitor experience into stronger accommodation demand. In GBR’s 2025 hotel sample for Nafplio, occupancy reached 45%, broadly stable compared with 2024, while ADR increased by 8.9% to € 88 and RevPAR rose by 9.2% to € 40.

Performance growth was therefore mainly rate-driven, while occupancy remained modest. Demand during the winter period, particularly from November to March, remains weak.

In Q1 2026, compared with Q1 2025, occupancy increased notably in January and February, albeit from a low base, while March recorded a mild decline. ADR increased by 2.1% year-on-year.

The main improvement areas identified by visitors are typical for historic destinations with compact urban cores. Parking, noise, traffic conditions, pavements and accessibility received among the lowest satisfaction scores. Activities, events and information on special events also show room for improvement. Addressing these issues would not only enhance the visitor experience but could also support longer stays, repeat visitation and stronger off-season demand.

Nafplio therefore illustrates the opportunity for many Greek destinations outside the country’s main tourism poles. The product is attractive, satisfaction is high and the source-market base is balanced. The next challenge is to convert this appeal into stronger annual demand through coordinated destination management, better event programming, more bookable experiences and targeted promotion to suitable domestic and international segments.

Selected transactions

At the end of April 2026, Fais Holdings S.A. signed a binding agreement for the sale of 100% of L.S. Santorini Kamari Hotel S.A., owner of the 5-star, 103-room Radisson Blu Zaffron Resort in Kamari, Santorini. The buyer is a joint investment scheme comprising four funds managed by Extendam and Redcliffe Capital. The total consideration amounts to € 28.3 million, including approximately € 16.8 million relating to assumed debt and other obligations. According to Fais Holdings, the transaction is expected to generate a profit of about € 5.5 million at Group consolidated level.

In April 2026, PHĀEA Hospitality Group and Hotel Investment Partners (HIP), backed by Blackstone and GIC, entered into a strategic agreement for Phāea Cretan Malia in Crete. Under the agreement, HIP acquired the 5-star, 204-room beachfront resort, while PHĀEA will retain the long-term management of the property. Since 2019, the resort has been a member of Design Hotels and carries Green Key and Travelife certifications. HIP is expected to invest further in the upgrading and repositioning of the property.

Domes Resorts agreed in April 2026 to acquire a majority stake in Casa Collective from investment funds linked to Goldman Sachs. Casa Collective is the hospitality platform behind the Cook’s Club, Casa Cook and XIA brands. Entrepreneur Remo Masala, creator of the Cook’s Club and Casa Cook concepts, will also participate as shareholder and strategic partner. The transaction is primarily a brand and platform acquisition rather than a single-asset hotel sale, and supports Domes Resorts’ international expansion strategy. Casa Collective will continue to operate as an independent hospitality company.

In March 2026, Greek business press reported that the Multi-Member Court of First Instance of Kos ratified the restructuring agreement of G. Kypriotis & Sons S.A., providing judicial confirmation to the transfer of the five Kipriotis hotels in Kos to Kos Holdings, linked to H.I.G. Capital. The ownership transfer had already been reported in June 2025 and covered in our Q2 2025 newsletter.

During the same month, H.I.G. Capital and its affiliates completed a $ 1.6 billion recapitalisation of Ella Resorts and OB Streem, with the refinancing arranged by a consortium of European banks.

Download in PDF format (260 kb)